Systemically Important Authorized Institutions (SIBs) are banks whose impact, in the event of distress or failure, could cause significant disruption to the financial system and ultimately, the broader economy. In recognition of the additional risks posed by SIBs, they are subject to specifically tailored regulatory and supervisory measures, including capital surcharges in the form of higher loss absorbency (HLA) capital buffers; more intensive supervision (particularly in areas such as risk management and governance) and prioritised recovery and resolution planning.

The Monetary Authority is empowered under the Banking (Capital) Rules to designate authorized institutions (AIs) incorporated in Hong Kong as global systemically important AIs (G-SIBs) or domestic systemically important AIs (D-SIBs) (collectively as SIBs) and to determine the associated HLA requirements. The assessment methodology to identify G-SIBs adopts the Basel Committee on Banking Supervision’s (BCBS) G-SIB framework. Currently there is no G-SIB headquartered and incorporated in Hong Kong.

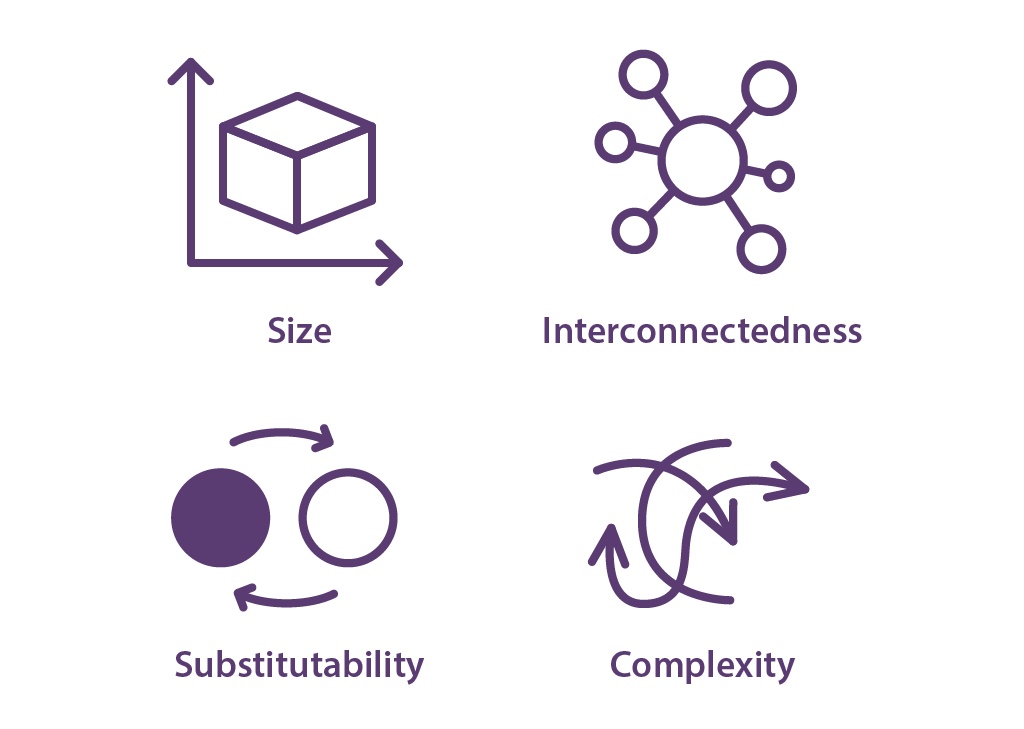

The D-SIB framework in Hong Kong is based on the four assessment criteria drawn from the BCBS’s D-SIB framework, namely size, interconnectedness, substitutability and complexity. The identification of D-SIBs locally consists of a two-step process. The first step is to draw up a preliminary indicative list of D-SIBs based on the quantitative scores calculated using the factors and a set of indicators. The second step involves the exercise of supervisory judgement to serve as a complement to the quantitative assessment process.

Four Assessment Criteria of D-SIB Framework

HLA requirements must be met with Common Equity Tier 1 capital. Depending on the systemic importance of the AI designated as a D-SIB or G-SIB, the HLA requirement ranges from 1% to 3.5% of an AI’s total risk-weighted assets (as calculated under the Banking (Capital) Rules).

The HLA requirement, together with the Countercyclical Capital Buffer (if applicable), takes effect as an extension of the Basel III Capital Conservation Buffer. Accordingly, if and when a SIB’s Common Equity Tier 1 capital ratio falls within the extended buffer range, the SIB will be subject to restrictions on the discretionary distributions it may make (including by way of dividend, share buyback, discretionary coupon payments on capital instruments and discretionary bonus payments to staff) according to a specified scale as set out in section 3H(1) of the Banking (Capital) Rules. The effect of this is that SIBs will be required to retain earnings in order to bolster their regulatory capital.