(Translation)

As we usher in the new year, I would like to take this opportunity to review the challenges faced by investors in 2016 and share with you the investment outlook and the strategies deployed by the Exchange Fund.

On the face of it, market conditions in 2016 appeared to be calmer than in the previous two years. But in reality, it was full of surprises, particularly in the second half of the year when unexpected events came one after another. The results of the Brexit referendum in June and the US presidential election in November took the market completely by surprise. However, it is pleasing to note the initial knee-jerk reactions were short-lived and financial markets quickly recovered lost ground. While many professional investors thought equity markets in the UK and the US would plunge, the FTSE 100 and the S&P 500 actually rose, both gaining about 10% for the whole year and among the best performers in 2016. Even if investors had a crystal ball and were able to foresee these “black swan events”, they might not have been able to predict that the market response would be another “black swan”! With such dramatic changes, even professional investors would have found it hard to make a profit.

The “black swan events” inevitably result in short-term fluctuations. But the more important point to note is that financial markets have been highly uncertain in the post-quantitative easing (post-QE) era. Major central banks have been pumping money into the financial systems since the global financial crisis. This has created serious imbalances and led to high volatility in the financial markets. In particular, investor speculation on changes to QE policies has often triggered sharp market fluctuations. For example, in the first three quarters of 2016, due to unstable global economic conditions, the US Federal Reserve kept interest rates on hold, while the European Central Bank and the Bank of Japan expanded their QE programmes, leading to market expectations of continued liquidity support by various central banks. However, entering the fourth quarter, with heightened market expectations of US interest rate hikes and the absence of new QE measures by other major central banks, bond yields surged and bond prices fell correspondingly. This, coupled with the strengthening of the US dollar, created a very challenging investment environment for the Exchange Fund in the fourth quarter. In fact, the market fluctuations experienced in the fourth quarter last year were simply a continuation of the three major challenges mentioned in my inSight article published in October 2015, namely, low returns and high volatility, the reducing complementary effects of bonds and equities, and a strong US dollar. These three major challenges are expected to continue to be the dominant forces shaping the investment landscape in the foreseeable future.

Low Return

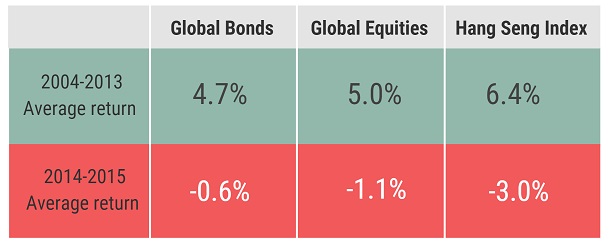

QE in various countries has created an ultra-low interest rate environment. With the substantial reduction in interest income, investors virtually had no other choice than to turn to more risky assets in pursuit of higher returns. As a result, asset bubbles which have been building up for a long time continue to expand, and the valuations of both the bond and equity markets have been relatively stretched. Fewer quality investment opportunities have also suppressed returns. How unsatisfactory were the returns of various asset classes in the past few years? As shown in the table below, global bond and equity indices recorded negative returns in 2014-2015. The Hang Seng Index also recorded an average annual drop of 3% during the same period. The performance of all three indices was far worse than that in the preceding 10 years (2004-2013).

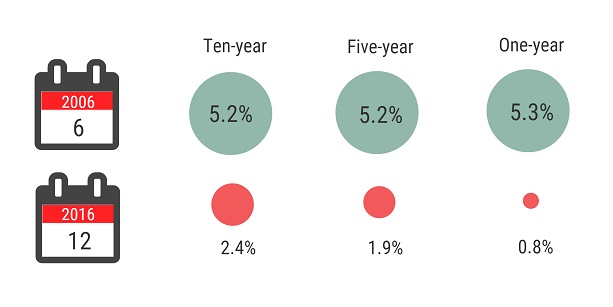

Although the US Treasury yields have begun to rise, the sharp fall in the yields in the past 10 years has created a major challenge to us. For example, the 10-year US Treasury yield was a meagre 2.4% at the end of 2016, and for most of the year it only hovered around 1.5-1.8%. Compare this with 5.2% in June 2006! Considering that the Exchange Fund’s bond portfolio totalled some HK$2.8 trillion at the end of 2015, a rough estimation suggests that the three to four percentage point difference represents a reduction of almost HK$100 billion in interest income annually!

A sharp fall in the US Treasury yields in the past 10 years

High volatility and strong US dollar

Global asset markets have been exceptionally volatile in recent years. Whenever there was a major event, such as increased market concerns over a slowdown in Mainland China’s economic growth and the reform of the renminbi exchange rate regime in 2015, the Brexit decision in June 2016 and Donald Trump’s victory in the US presidential election in November 2016, the Chicago Board Options Exchange Market Volatility Index (VIX), an indicator of investor sentiment or often referred to as “fear gauge”, would surge. This reflected investors’ high sensitivity to unexpected incidents. In general, while global equity markets performed well in 2016, the prices of various assets experienced big swings during the period. Some assets sensitive to interest rate movements, such as bonds and emerging market assets, experienced sharp adjustments in the last two quarters of 2016. The 10-year US Treasury yield, after falling to a record low of 1.36% in July, shot up by more than 120 basis points to 2.60% in mid-December. The MSCI Emerging Markets Index had also once dropped nearly 10% from a high level during the fourth quarter. The foreign exchange market was equally volatile. The US dollar index rose to its highest level in 14 years at the end of last year, while other major currencies have depreciated sharply. For example, the British pound depreciated by 16% against the US dollar during the year, posting its biggest fall since 2008. Meanwhile, crude oil futures prices in New York increased about twofold to US$54 a barrel at the end of the year from a low of US$26 a barrel at the beginning of 2016.

Reducing complementary effects of bonds and equities

Conventional wisdom has it that equity and bond prices move inversely in turbulent times. This “equities down, bonds up” pattern suggests these two types of assets are complementary to a large extent. Simply put, when equity markets fall, gains in bonds can help offset equity losses. However, as returns from bonds and equities have become increasingly synchronised in recent years, the effectiveness of risk diversification through an equity-bond portfolio mix has weakened considerably. More recently, with market expectations that Donald Trump’s favourable stance towards the commercial sector and his fiscal stimulus package will benefit the equity market and push up inflation expectations, equity prices and bond yields have risen concurrently, leading to a recurrence of the “equities up, bonds down” pattern. Nevertheless, there are still considerable uncertainties regarding whether the new US administration will implement its policies as intended, how the policies will be implemented, and whether inflation expectations will surge too quickly. Therefore, it remains to be seen whether the complementary effect is just a short-lived phenomenon or a revival of the conventional trajectory.

A complex and unpredictable future

In the foreseeable future, financial markets are expected to be plagued with geopolitical risks. There are great uncertainties over the policy direction of the new US administration and its ability to implement the policies, the progress of Brexit and national elections in a number of European Union member countries. At the same time, the US monetary policy is at a turning point, while the policies of other major central banks are becoming more uncertain. It is inevitable that financial markets will continue to be volatile. In such an environment, many institutional investors, including sovereign wealth funds and large asset management companies, anticipate that low returns, high volatility and high risk will continue to dominate the investment landscape. In my next inSight article, I will discuss how the Exchange Fund will strive for stable returns in such a difficult investment environment.

Eddie Yue

Deputy Chief Executive

Hong Kong Monetary Authority

09 January 2017