In Hong Kong, household debt as a percentage of gross domestic product (GDP) has been on the rise, and the pace has quickened last year. This has raised some concerns and discussions in the community. While the underlying reasons for this phenomenon are quite technical in nature, in this inSight article I will try to offer a simpler way to help readers better understand what explains the rise in household indebtedness in Hong Kong.

Let us first understand the concept of household debt-to-GDP ratio. This is a simple and widely used measure for gauging the financial soundness of households. It is similar to the concept of household debt-to-income ratio, but for ease of comparison across economies, the household debt-to-GDP ratio is constructed using more readily available data. Specifically, the ratio uses as its numerator the gross debt outstanding of households (instead of net household liabilities which take into account household assets). For the denominator, the ratio uses nominal GDP as a proxy for the gross income of the whole economy.

This simple measure allows analysts to easily gauge and compare the household debt burden across different economies. However, it does not represent the actual household debt-to-income ratio within the economy. To more objectively assess the risks associated with household indebtedness and its implications for banking stability and the broader economy, we need to examine a number of other factors.

Firstly, we see that household debt as a proportion of GDP has risen significantly in the past year. This was primarily due to the economic contraction in Hong Kong that has been taking place since 2019. In 2020, amid the COVID-19 pandemic, Hong Kong’s GDP recorded the sharpest fall in history, with nominal GDP dropping by 5.4%. As such, even though the pace of household debt growth moderated to 5.5% in 2020 (compared with 12.8% in 2019), the fall in GDP continued to push up the household debt ratio by almost 10 percentage points.

Some of you may wonder why a decrease in income would not lead to a corresponding fall in household debt. The truth is, the numerator in this ratio is outstanding household debt, which is the debt accumulated to date. In a weakening economy, people at the risk of losing their jobs are unlikely to repay their old debts early. Thus, it is quite normal to see sharp GDP falls driving up the household debt-to-GDP ratio during an economic downturn. This is observed not only in Hong Kong but also in the US, the UK, Japan and other economies.

To fully understand what lies behind the continued rise in Hong Kong’s household debt-to-GDP ratio in the past few years and its implications for financial stability, we should first look at the composition of household debt. Currently the majority of household debt in Hong Kong is made up of residential mortgage loans (68%) and loans for other private purposes (27%), while credit card advances account for only a small portion (5%). Among these components, residential mortgage loans have been on an upward trend amid strong housing demand. However, with countercyclical measures in place, residential mortgage loans have grown at a much slower pace than property prices. Since 2009, residential mortgage loans have grown by 1.6 times, compared to the 2.5 times increase in property prices. As for loans for other private purposes, most are secured lending to private banking customers. The continued growth in these loans mainly reflects the rapid expansion of private banking business as Hong Kong develops into a global wealth management centre. The appreciation in asset prices over time has also contributed to the increase in these loans.

As most of the loans used for financing home purchases or investments are pledged with underlying assets, the associated credit risk to banks is lowered. Compared to other places in Europe and the US, consumer credit (such as credit card advances) makes up only a small portion of household debt in Hong Kong. This type of lending is generally not secured by assets and may expose banks to greater credit risk when borrowers’ income declines during an economic downturn. Since most household debt in Hong Kong is investment-related collateralised loans, the credit risk to banks in Hong Kong amid an economic downturn is relatively low.

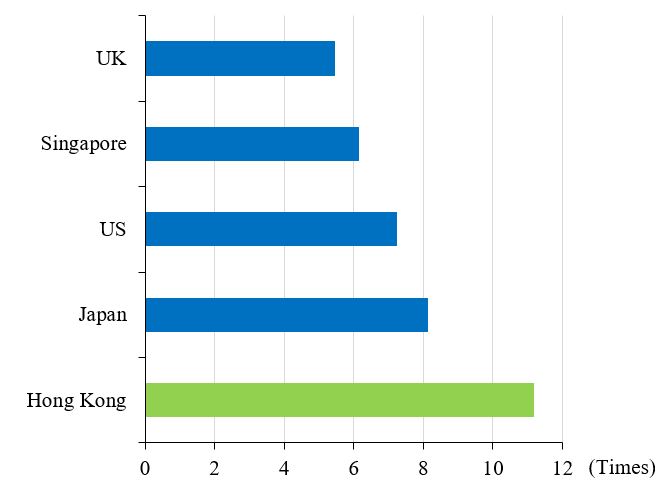

Furthermore, one cannot assess the financial robustness of households based on the household debt-to-GDP ratio alone. We also need to look at the asset side of the household balance sheet, and consider indicators such as the assets-to-liabilities ratio, asset quality, and so on. According to our estimates, total deposits of the household sector in Hong Kong (i.e. household assets unaffected by asset prices) are a good three times of its total liabilities. Compared with other major economies, such as the UK, the US and even Japan, Hong Kong has the highest household net worth-to-liabilities ratio (Chart 1).

Prudent credit risk management, which has prevented excessive borrowing, has been the reason behind the good financial health of the overall household sector in Hong Kong. Following the HKMA’s multiple rounds of countercyclical macro-prudential measures since 2009, the average loan-to-value ratio and average debt servicing ratio of new residential mortgage loans have stayed at healthy levels. In turn, this has strengthened the resilience of both households and the banking sector against possible downturns in the property market.

As for loans to individuals, the HKMA has always required banks to adopt prudent and effective credit risk management measures, including imposing a prudent cap on loan-to-value ratios for financial assets pledged as collateral and implementing effective mechanisms on margin calls and forced liquidation, for lending secured by various types of financial assets. These measures are strictly followed by banks. As for unsecured consumer credit, the HKMA also requires banks to operate their credit card advance and personal loan businesses with prudence, and to carefully assess the borrowers’ repayment ability when processing loan applications. Banks are also required to implement effective post-lending monitoring, including regular assessments of the asset quality of their loan portfolios.

Thanks to these prudent credit risk management measures, banks in Hong Kong have weathered through numerous economic downturns and maintained good asset quality.

Given the above, we consider that the credit quality of local household debt has held up well and the overall financial position of the household sector remains robust. While we expect the household debt-to-GDP ratio to remain elevated in the short term due to cyclical and structural factors, we believe the overall risk of household debt in Hong Kong is manageable. As always, the HKMA will continue to ensure that banks approve loan applications prudently and closely monitor any changes in the quality of their loan portfolio.

Edmond Lau

Senior Executive Director

Hong Kong Monetary Authority

30 March 2021

Chart 1

Household net worth-to-liabilities ratio

Note: The Japan figure is from end-2018, while the figures for the other economies are from end-2019.

Sources: HKMA staff estimates, and statistical agencies or central banks of selected economies.