Looking back, it has been more than five years since I last went to a bank or used an ATM to make a fund transfer. The launch of the Faster Payment System (FPS) in September 2018, which achieved full connectivity among banks and stored value facilities (SVFs), has enabled instant interbank transfers with just a few taps on mobile devices. Gone are the days when I had to go through the hassle of queueing up to make a fund transfer.

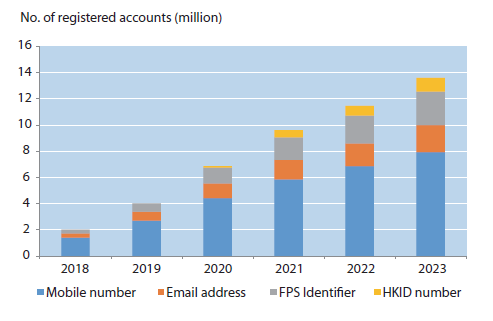

Since the launch of the FPS, the number of FPS registrations1 grew from over 2 million at the end of 2018 to 13.6 million at the end of 2023 (Exhibit 1), marking an average annual growth of 46% and almost doubling the population of Hong Kong2. Mobile number is the most popular account proxy. Currently, there are about 4.4 million mobile numbers linked to over 7.9 million accounts, meaning that each mobile number is linked to nearly two different banks or e-wallets on average. In fact, around 180,000 users have linked their mobile numbers to five or more accounts, probably to facilitate fund transfers between their own accounts more conveniently. In addition, the account proxies of email address and the FPS Identifier recorded over 2 million and 2.5 million registrations respectively.

The Hong Kong Identity Card (HKID) number account proxy, which is used to receive payments from institutions, has over 1 million registrations. One use case is for companies to pay salaries to employees via the FPS using their HKID numbers, such that employees may choose to change their payroll accounts anytime without bothering their employers. Not only is the arrangement convenient to employees, it also reduces the administrative workload of employers. The HKMA has already offered this option to its staff members and many of our colleagues are using it.

Gradually expanding applications to meet daily payment needs

The FPS has become an integral part of our daily lives, from splitting the bill when eating out with friends to paying household expenses to family members. It can also be used to pay utility bills, taxes, rates and Government rent as well as fees for leisure facilities, tunnels, parking meters, public hospitals and rental of public housing and retail space. Currently, more than 90% of Government departments accept the FPS as a means of payment. Moreover, the FPS can also be used for making payments for in-store or online shopping, dining out, driving lessons, school fees, video game top-ups, donations and even consultations at some Chinese medicine clinics, reflecting the popularity of the FPS in our everyday lives.

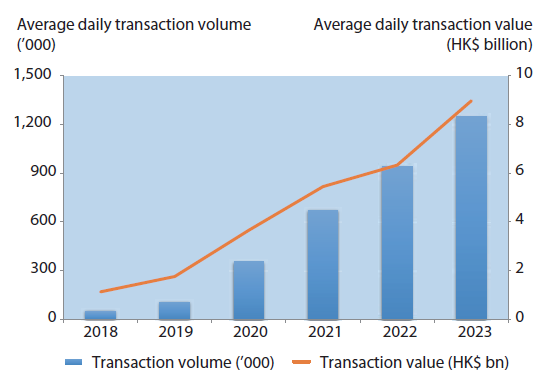

We are pleased to see that the usage of the FPS has been gradually expanding in the past five years. While person-to-person payments accounted for over 90% of the transactions at the beginning, e-wallet top-ups, bill payments, merchant payments and business payments now collectively make up 50% of the turnover. This includes many small and medium-sized enterprises (SMEs) and merchants which have adopted the FPS to enhance operational efficiency and reduce administrative work, thereby supporting them in embracing the era of e-payment and strengthening their competitiveness. These developments have helped the turnover of the FPS to rise steadily (Exhibit 2), maintaining a double digit annual growth since its launch five years ago. In 2023, the average number of transactions reached 1.25 million per day, representing an average annual growth of 64% since the first full year of operation of the FPS in 2019. The average daily value of Hong Kong dollar transactions was HK$9.0 billion, marking an average annual increase of 38% since 2019.

Strengthening the functions of the FPS and enhancing user experience

In addition to expanding the applications of the FPS, we are also upgrading its functionality continuously so as to enhance user experience. For example, the App-to-App and Web-to-App payment functions were introduced to enable users to make payments with their mobile phones more efficiently and conveniently.

The FPS processes over one million real-time transactions daily. While the FPS offers convenient payment services to the public, the associated fraud risks cannot be overlooked. To address the threat of fraud, the HKMA, in collaboration with the Hong Kong Police Force, the Hong Kong Interbank Clearing Limited and the industry, launched the Suspicious Proxy ID Alert last year. The initiative aims to better protect the public by mitigating the associated fraud risks when making payments using FPS proxy IDs.

Transcending boundaries

With the development of the FPS in Hong Kong becoming increasingly mature, we have been actively exploring opportunities to establish linkages with different jurisdictions. In December 2023, the FPS successfully established its first overseas linkage and jointly launched the “FPS x PromptPay” with the Bank of Thailand, marking its first step for cross-border payments. In January this year, just two months after the launch of the service, Hong Kong ranked third based on the payment volumes among Thailand’s cross-border QR payment corridors, behind Malaysia and Indonesia which had far more visitors to Thailand than Hong Kong3. Clearly this new service is gaining popularity among Hong Kong people, with noticeable surges in transaction volumes seen during weekends and long holidays.

Recently, I have also visited Thailand to gain first-hand experience of this new service. Besides shopping and dining, I found it particularly convenient to buy Bangkok BTS Skytrain tickets by scanning the PromptPay QR code. I no longer need to wait in line to change for coins for ticket purchases. The transaction was completed in seconds, which suits the fast-paced lifestyle of Hong Kong people. Currently, the linkage is mainly used for small value retail payments with the average transaction value below HK$200, but there are also some higher value transactions such as payments for fine dining, dental care and golf lessons, with the highest single transaction value reaching almost HK$10,000. This linkage with Thailand has established a strong foundation for us to further explore the potential of similar collaborations with other jurisdictions.

Meanwhile, we have been working closely with the Digital Currency Institute of the People’s Bank of China to further expand the cross-boundary e-CNY pilot in Hong Kong. With the completion of a drill that involved various Mainland operating institutions and Hong Kong banks in early 2024, the e-CNY pilot is expected to further expand its scope in Hong Kong to facilitate the set up and usage of e-CNY wallets by Hong Kong residents as well as top-up through the FPS. This arrangement will facilitate cross-boundary retail payments of both Hong Kong and Mainland residents, thereby supporting payments in the “one-hour living circle” in the Guangdong-Hong Kong-Macao Greater Bay Area.

Forging ahead and keeping pace with the new era

The FPS was built to enable fund transfers between banks and SVFs. Today, the FPS has evolved to become an integral part of our daily lives and has even ventured into cross-border use. The wide adoption of the FPS achieved over the past five years would not have been possible without the support of the industry, which has been working closely with the HKMA to develop new use cases and enhance system functionalities. Fintech advances by leaps and bounds. We will keep monitoring market developments and needs and explore further opportunities. With this solid foundation, we hope that the FPS will forge ahead to explore new frontiers.

Howard Lee

Deputy Chief Executive

Hong Kong Monetary Authority

27 March 2024

Note: For more details, please click the link below to access the feature article on the FPS.

The Faster Payment System: A Five-Year Journey of Innovation and Growth

Exhibit 1: Number of FPS registrations

Exhibit 2: Average daily turnover of Hong Kong dollar real-time payments in the FPS

1 The public can register with the FPS using their mobile number, email address, FPS Identifier and HKID number. The number of registrations is not equivalent to the number of users as a user can register with more than one account proxy (e.g. mobile phone number and email address) and link to one or more bank accounts or e-wallets.

2 According to the Census and Statistics Department, the population of Hong Kong as at end-2023 was 7.5 million.

3 The number of travellers from Malaysia and Indonesia to Thailand in January were around 7 times and 1.5 times that of Hong Kong respectively.